The 2020 COVID-19-induced pandemic and resulting recession created turmoil in the multifamily market; however, there was less disruption than expected because many renters were able to telecommute or quickly return to work and continue to pay their rent. In addition, some renters moved from more expensive, densely populated urban submarkets to less expensive suburban submarkets but remained in the same metro.

We believe that the multifamily vacancy rate only grew by half a percent in 2020 to 6.0%, bringing it back to its long-term average, and rents overall declined by less than 1 percent in 2020. Even with these changes, long-term affordability issues affecting renters remain firmly in place and have been exacerbated in some metro areas.

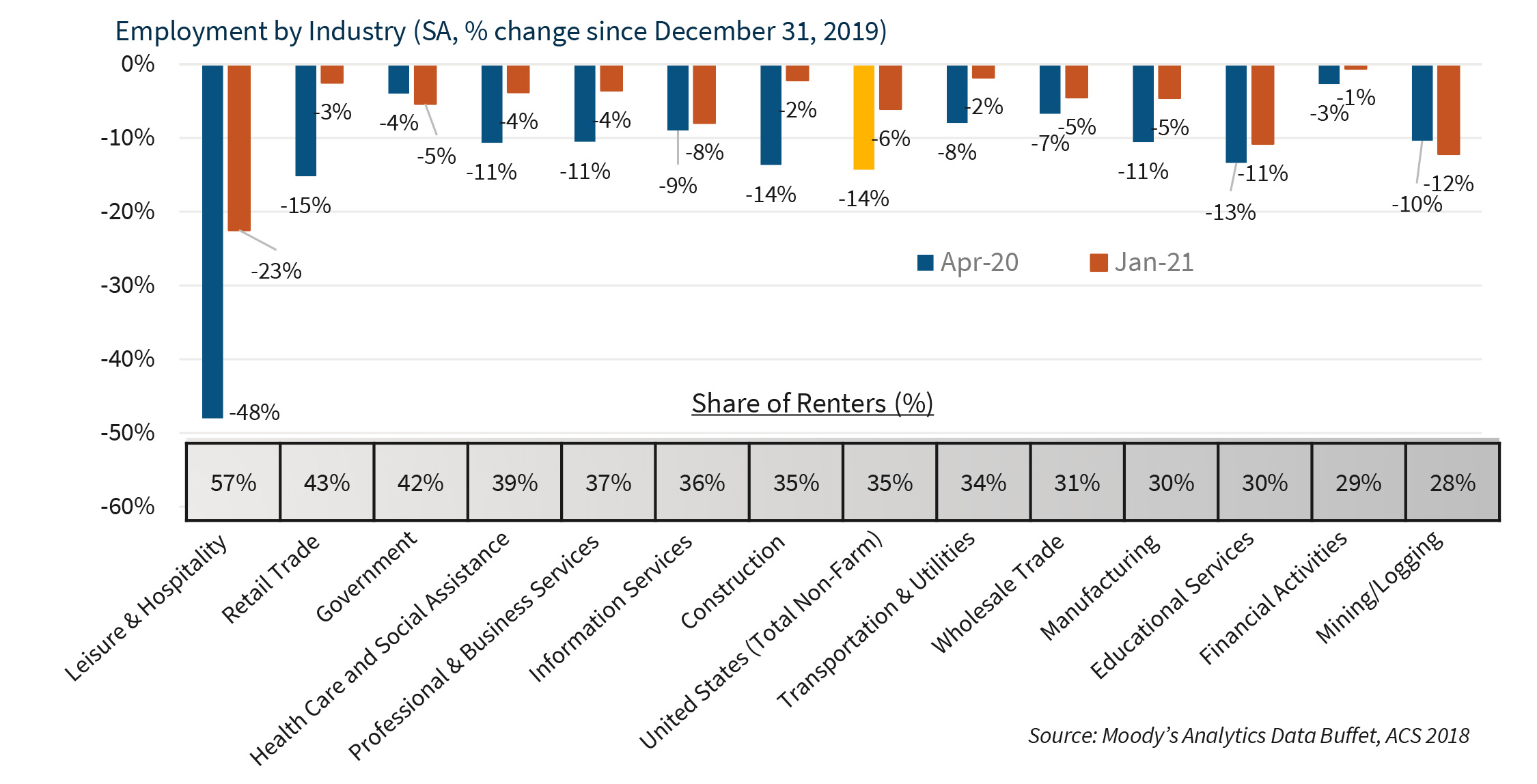

Workers in Affected Job Sectors Tend to Rent

The job sectors that lost the most jobs due to the pandemic and have not yet recovered were in sectors reliant on people gathering in close proximity. For example, as of the end of January, there are still an estimated 23% fewer jobs in the Leisure and Hospitality sector than there were at the start of 2020, representing a 3.8 million job loss in this sector alone.

More importantly, these are also the workers most likely to rent. As recently as 2018, an estimated 57% of workers in the Leisure and Hospitality sector were renters, as seen in the chart below. Lower income workers who rent need lower rent apartments, which are generally provided by Class C rentals. However, even with the effect of the pandemic, changes in Class C fundamentals have not benefitted lower income renters overall.

Minimal Increase in Class C Vacancy...

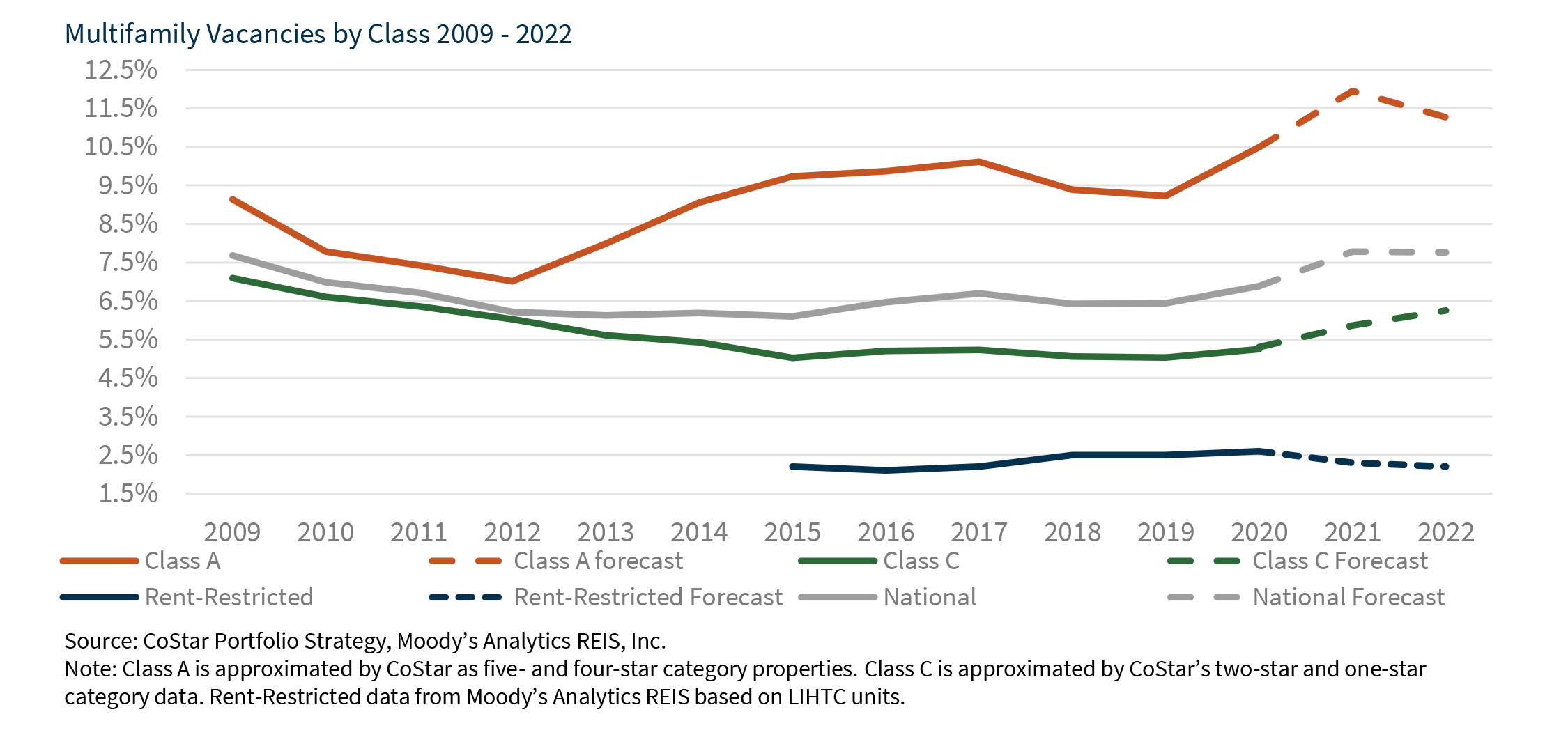

Class C apartment units, which are considered the most affordable units available in a market, have barely seen an uptick in vacancies during the pandemic. According to CoStar, the national average vacancy rate for Class C units, which has hovered around 5.0 percent since the end of 2015, increased just 30 basis points during 2020, ending the year at an estimated 5.3 percent. In contrast, CoStar estimates that the average vacancy rate for Class A units, which are considered the most expensive units available in a market, and which have seen an influx of new supply in certain locations over the past few years, ended 2020 with an average vacancy rate of 10.5 percent, almost twice as high as Class C units. In addition, vacancies for properties assisted by federal Low Income Housing Tax Credits (LIHTC) had an even lower vacancy rate at just 2.6 percent, according to estimates from Moody’s Analytics REIS.

The minimal increase in the average estimated vacancy rate for Class C units can be attributed to a combination of factors. There has been little increase in the supply of Class C units, and it is generally infeasible from an economic standpoint to build new units without local subsidies or federal assistance to keep the rents affordable. Continued demand for multifamily rentals has made older Class A and B units more attractive to investors as value-add projects, keeping them from naturally filtering down to Class C. Lastly, stimulus payments and eviction moratoriums have helped renters stay in their more affordable units, keeping vacancy levels low.

...and Expected to Stay That Way

As shown in the chart above, CoStar projects that the average 2021 vacancy rate for Class A units will increase by an estimated 1.5 percent this year, peaking at 12 percent, due to continued deliveries of new supply. In contrast, CoStar projects the average vacancy rate for Class C units will rise by 1.0 percent, ending 2022 at an estimated 6.3 percent, still well below its estimated 7.1 percent average Class C vacancy rate in 2009 at the end of the Great Recession.

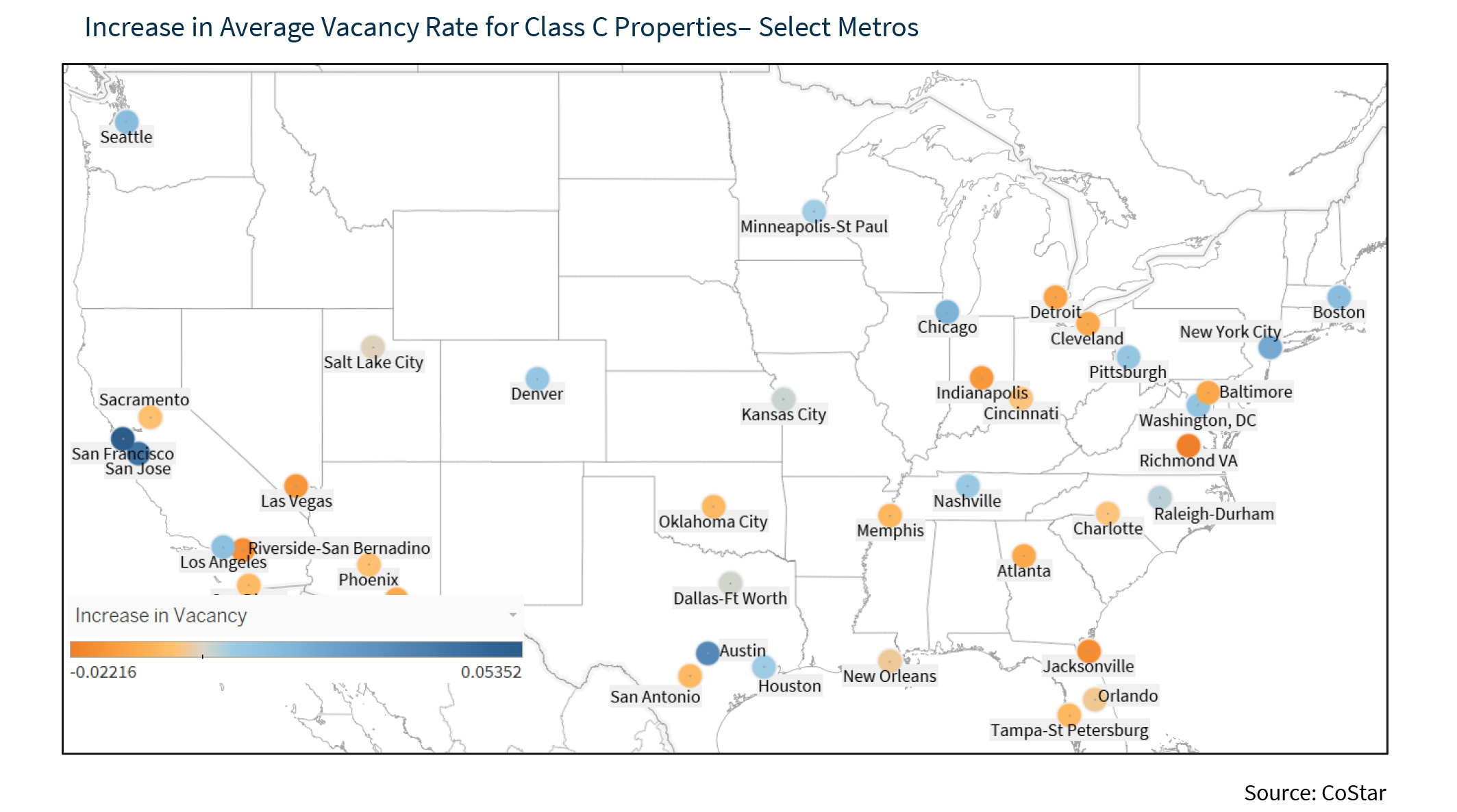

However, it’s important to note that there has been quite a bit of variation in the average Class C vacancy rate across various metro areas.

Class C Vacancy Rates Increased in Higher-Cost Locations...

According to data from CoStar, Class C vacancy rates increased in more expensive urban submarkets with high rates of COVID cases as residents moved to less expensive areas with the potential for larger but more affordable units. As shown on the map above, the highest increase in vacancy occurred in high-cost metros, such as San Francisco and San Jose, both of which had an increase of more than 4.0 percent, bringing their average Class C vacancy rates to over 8.6%. Similarly, Class C vacancy rates increased by nearly 2.0 percent in New York to 4.5 percent, and by just over 1.0 percent in Seattle to an estimated 5.6 percent, according to CoStar.

...but Tightened in More Affordable Markets...

By contrast, Class C vacancy rates fell in many metros that are more affordable. For instance, the average Class C vacancy rates in Riverside/San Bernardino and Sacramento fell by 1.8 percent and 0.5 percent, respectively, in 2020 to just 2.3 percent and 3.2 percent, respectively, according to CoStar.

The average Class C vacancy rates also declined in many metros in the South and Southwest, based on a continuing long-term migration pattern to these areas. For instance, the average vacancy rate in Tampa and Charlotte fell by 1.9 percent and 0.8 percent, respectively, to just 4.5 percent and 5.5 percent, respectively. Meanwhile, the average vacancy rate in Phoenix and Las Vegas fell by 0.5 percent and 1.6 percent, respectively, to average vacancy rates of 5.7 percent and 5.8 percent, respectively, based on CoStar data.

Other metros experiencing declines in Class C vacancy rates in 2020 were midwestern metros that have not seen much new supply in recent years, thereby keeping supply levels stagnant. Some metros in this category include Detroit and Cleveland, which saw their average Class C vacancy rates decline by just over 1.1 percent in 2020 to 4.6 percent and 5.4 percent, respectively, according to data from CoStar.

...with a Couple of Notable Exceptions

A couple of traditionally more affordable metros bucked this tightening trend. According to CoStar, Austin ended 2020 with an average vacancy rate over 9 percent after recording a large 3.3 percent increase in its average Class C vacancy rate. Houston ended 2020 with an average Class C vacancy rate over 10 percent even after a more modest increase of 0.5 percent. Both metros have had a substantial amount of Class A units delivered over the past few years. As a result, it appears that renters that were able to pay their rent could afford newer units, creating a cascading move-up effect.

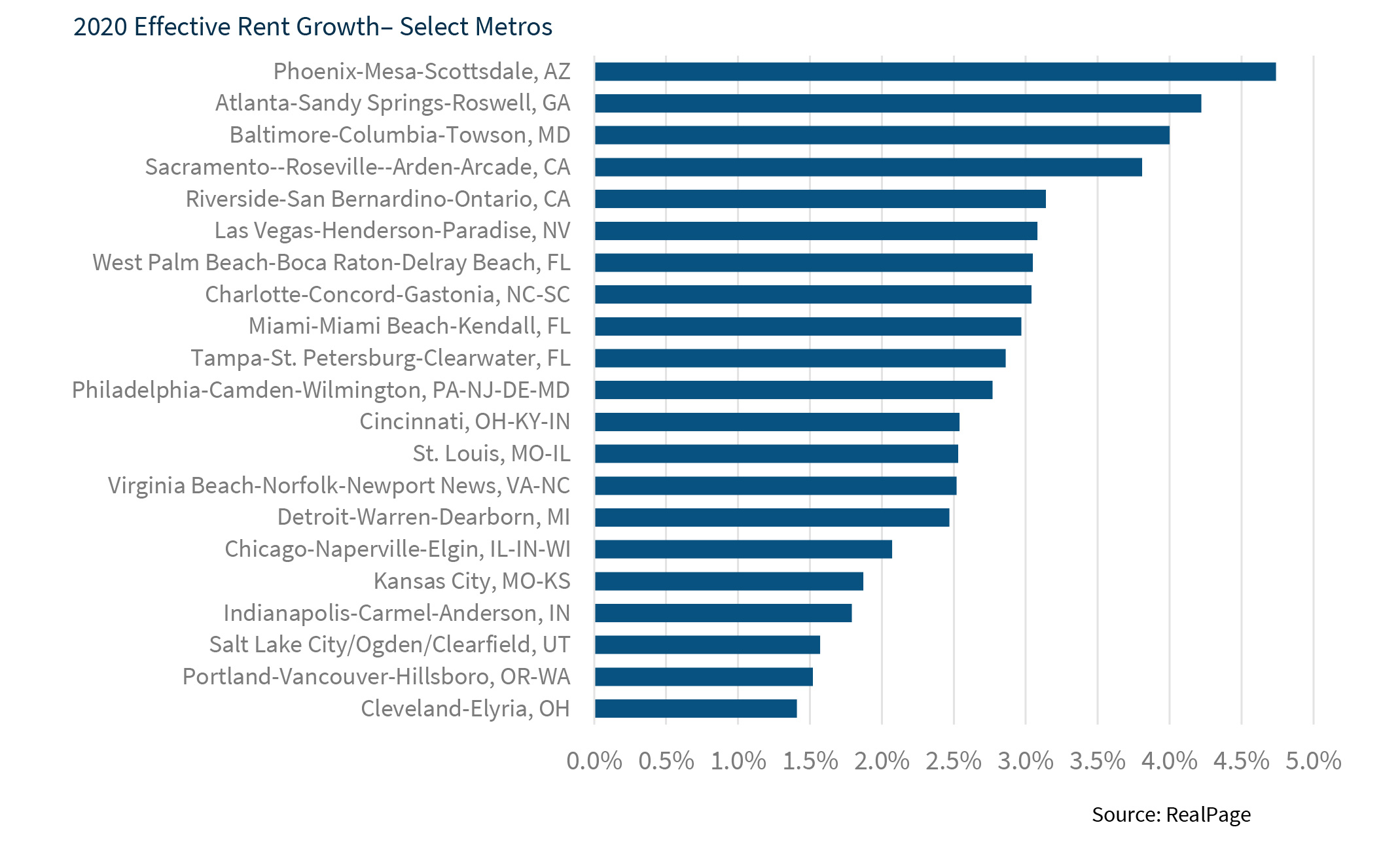

Tightening Vacancies Increase Pressure on Rents

Tightening vacancies have also led to an increase in rents for the most affordable apartments in some traditionally more affordable metros. According to data from RealPage, Inc., which defines Class C apartments as those in the bottom 20 percent of market rents for a given metro, rents have risen strongly in 2020 in several southern and southwestern metro areas. As shown in the table below, RealPage estimates that the average effective rents for Class C units in Phoenix, Las Vegas, Riverside/San Bernardino, and Charlotte have increased by 3.0 percent or more in 2020.

In addition, RealPage data shows that rents have continued to increase in many slower growth midwestern metro areas. For instance, the average effective rents in Cincinnati, St. Louis, Detroit, and Chicago all grew between 2.0 percent and 2.9 percent in 2020, according to RealPage. The combination of falling vacancies and rising rents in Class C units overall has exacerbated lack of housing affordability for the lowest income renters in these metros.

Rising Vacancies Do Not Always Lead to Affordable Rents

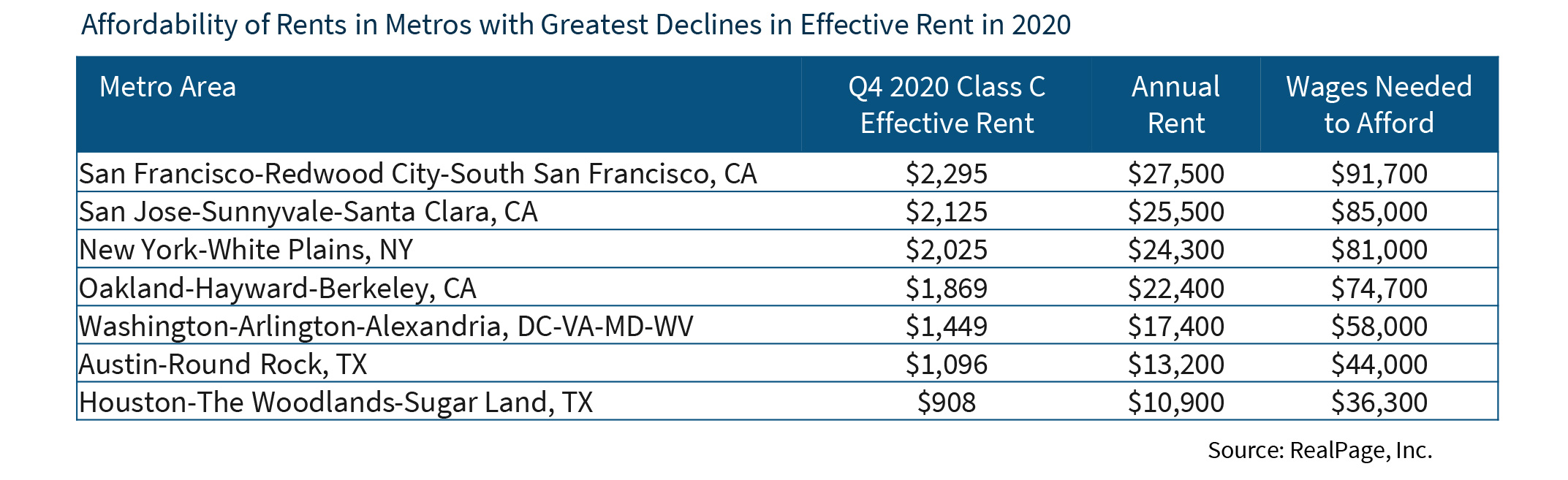

While vacancy rates increased dramatically in some higher cost metro areas in 2020, this did not necessarily lead to substantial improvements in affordability for lower income renters. According to RealPage, average effective rents for Class C apartments fell by 3.0 percent or more in 2020 in San Francisco, San Jose, and New York, and by 1.5 percent in Washington, DC. However, rents remained classified as “unaffordable” in these locations, as shown in the table below. For instance, the average monthly effective rent for Class C apartments in the New York metro area was $2,025 as of fourth quarter 2020, according to RealPage. A renter would need to earn about $81,000 per year for this rent level to be considered affordable. The monthly effective rent for a Class C apartment in San Francisco was $2,295 in fourth quarter 2020, requiring an annual income of $91,700. Thus, even with the sharp decline in rents experienced in these metros, their estimated average Class C rent levels remain “unaffordable” for many lower income renters.

Lower Income Renters Struggle to Pay Rent

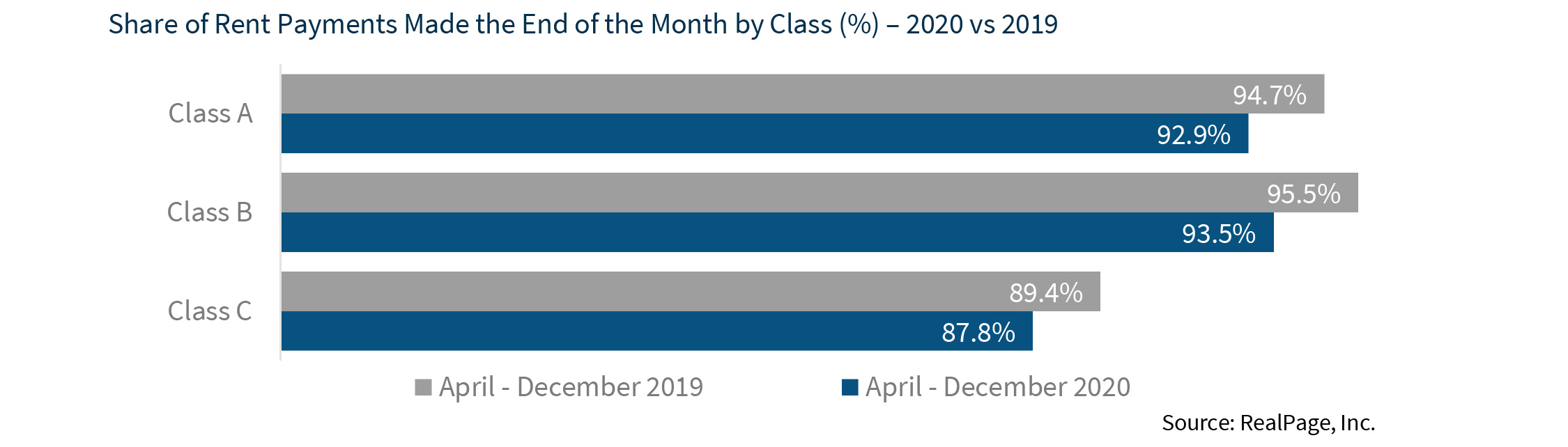

Even prior to the pandemic, lower income renters struggled to pay rent. As shown in the chart below, typical Class C rent payments between April and December 2019 trailed collections in Class A and B properties by between 5 and 6 percent. The share of rent payments made by Class C renters during this time period was estimated to be 89.4 percent, according to RealPage, compared to 94.7 percent for Class A units and 95.5 percent for Class B units.

With eroding affordability and job insecurity stemming from the pandemic, there is concern that the lowest income renters may be further impacted. There is some evidence that Class C renters are struggling more than usual as the share of Class C rent payments made from April to December 2020 fell by 1.6 percent compared to the same time period in 2019 to 87.8 percent of all Class C rental payments.

Federally Assisted Rental Housing Not Immune

Renters who receive federal assistance are among the lowest paid workers. In fact, just under 56 percent of renter households living in properties assisted with LIHTC, and 80 percent of renter households living in properties assisted by Project-Based Section 8 earn less than $20,000 per year. Except for the LIHTC program, renters under federal assistance programs generally spend no more than 30 percent of their household income on rent and utilities.

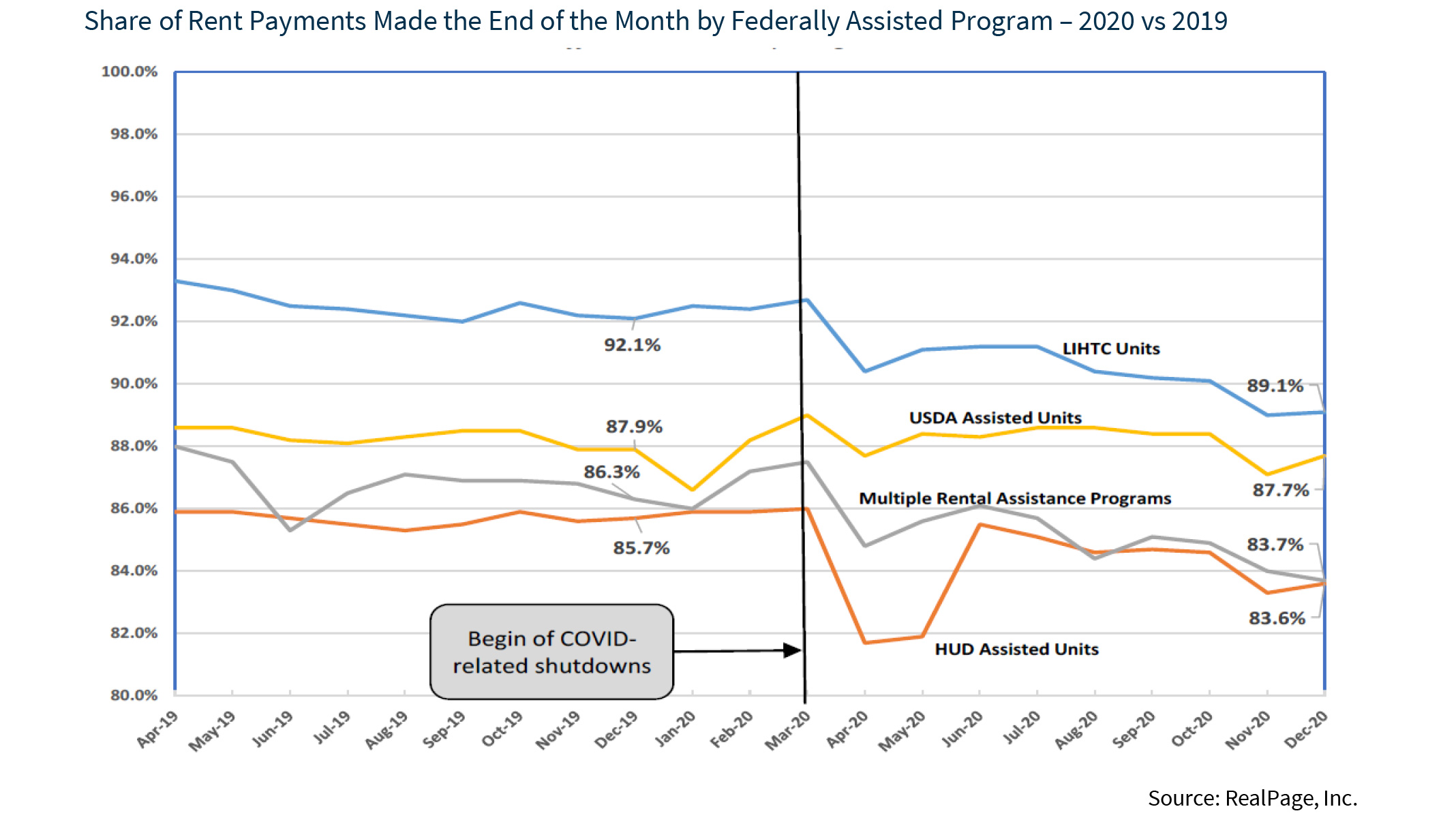

Even so, these renters are still at risk because most work to afford their rent. According to RealPage, the share of rent payments made at federally assisted properties declined to 86.3 percent in December 2020 from 88.8 percent in March, prior to the start of COVID-related shutdowns, which is a lower share of rents paid than estimated for Class C units. This trend may be due to the large share of renters earning less than $20,000 annually living in these properties, meaning any disruption to income could affect their ability to make the rent payment.

LIHTC Program Fares Better Than Average

Interestingly, the share of payments made varies by program, as shown in the chart above. According to the National Preservation Database, 49 percent of federally assisted rental homes receive LIHTC, making it the largest program providing federal assistance. An estimated 2.4 million units were assisted by LIHTC, as of June 2020.

Unlike most federally assisted programs, the LIHTC program does not guarantee that residents in these units will spend no more than 30 percent of their income on rent and utilities. In fact, according to the National Council of Housing Finance Agencies (NCSHA) 2018 State HFA Factbook, more than 25 percent of LIHTC-assisted units also receive assistance under the Project-Based Section 8 program.

Even so, the LIHTC program has fared better than average recently with an estimated 89.1 percent of rents paid by the end of the month in December 2020 compared to 86.3 percent for federally assisted programs overall. This appears to be higher than the 87.8 percent share paid in the Class C segment that does not receive federal assistance. Nevertheless, renters of LIHTC-assisted units appear to be struggling as their share of rents paid by the end of the month declined by 3.0 percent as of December 2020 relative to the share paid prior to March 2020.

More Supply Would Help Affordability

In 2019, just under a quarter of renters, representing 10.5 million renter households, spent more than half of their household income on rent and utilities, making them severely cost-burdened. Further, lower income renters were more severely cost-burdened: 43 percent of renters earning between $15,000 and $29,999 spent at least half of their household income on rent and utilities. As a result, additional supply affordable to low-income households is needed.

The fiscal year 2021 omnibus spending bill included a minimum 4% rate for the Low-Income Housing Tax Credit (LIHTC) program to support the supply of affordable units. Novogradac estimates that the new 4% minimum rate will finance an additional 130,000 rentals affordable to the lowest income households from 2021 through 2030. The legislation also included at least a $1.2 billion allocation of non-COVID disaster LIHTCs for 11 states and Puerto Rico. However, this allocation will likely replace supply lost rather than increase supply.

More Rental Assistance Would Help Lower-Income Renters

While more new supply would certainly help combat affordability issues, housing insecurity is also a significant issue. People facing housing insecurity may see some temporary relief as part of the federal government’s December 21, 2020 $900 billion coronavirus stimulus bill. This stimulus package will be administered by state and local governments and provides $25 billion in financial assistance to help those renters earning up to 80 percent of their local area median income that were impacted by the pandemic to pay past-due rent, coming rent, utility bills, or other housing expenses.

However, as the effects of the pandemic linger, and vaccinations take time to become more widespread, lower income renters are expected to be more severely impacted. As a result, many observers predict that they are likely going to need additional assistance to remain in their homes, at least over the short-term.

Tanya Zahalak

Senior Multifamily Economist

Multifamily Economics and Strategic Research

February 16, 2021

Opinions, analyses, estimates, forecasts, and other views of Fannie Mae’s Economic and Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae’s business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR Group bases its opinions, analyses, estimates, forecasts, and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current, or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts, and other views published by the ESR Group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.